Every operator who is growing says a version of the same sentence on the first call: we are always looking to lower our cost of goods. It is the most rational goal in the business. Food typically runs 28 to 35 percent of sales, and net margins sit somewhere around 3 to 5 percent, so a few points of food cost is often the entire profit line.

The problem is that the lever most operators reach for first, buying it cheaper, has quietly stopped working.

The Math You No Longer Control

Foodservice distribution has consolidated to the point where the negotiation is not really yours anymore. The largest distributor states in its fiscal 2025 annual report that it serves about 17 percent of an approximately $370 billion annual US foodservice market, and the top national players together control roughly a third of it, a share that has been climbing for a decade. When federal regulators blocked a proposed merger between the two largest distributors in 2015, they warned that foodservice customers would likely face higher prices and diminished service, because the combined company would have controlled roughly 75 percent of the national broadline market.

Then there is the contract. Multi-unit operators routinely lock into two- and three-year distribution agreements. Once the ink is dry, the price is whatever the schedule says it is, and a mid-sized operator has almost no leverage to reopen it mid-term.

Layer commodity inflation on top. The USDA’s 2026 Food Price Outlook projects food-away-from-home prices rising 3.6 percent and wholesale beef prices rising 9.4 percent this year, and the domestic cattle herd started 2026 at 86.2 million head, its smallest count in 75 years. You do not set any of those numbers.

The One Lever That Is Still Yours

If you cannot change the price per pound, the only variable left is the number of pounds. How much you buy, how much you prep, and how much you hold.

That is exactly where margin quietly dies. Over-prepping means high-value proteins get cooked and thrown away. Under-prepping means stockouts and lost sales at full menu price. And the operator who keeps the whole system in their head, spending ninety minutes a day guessing tomorrow’s prep, can make that work at one or two locations. It does not survive five more, especially across different concepts and demand that spikes around events no one can fully predict from memory.

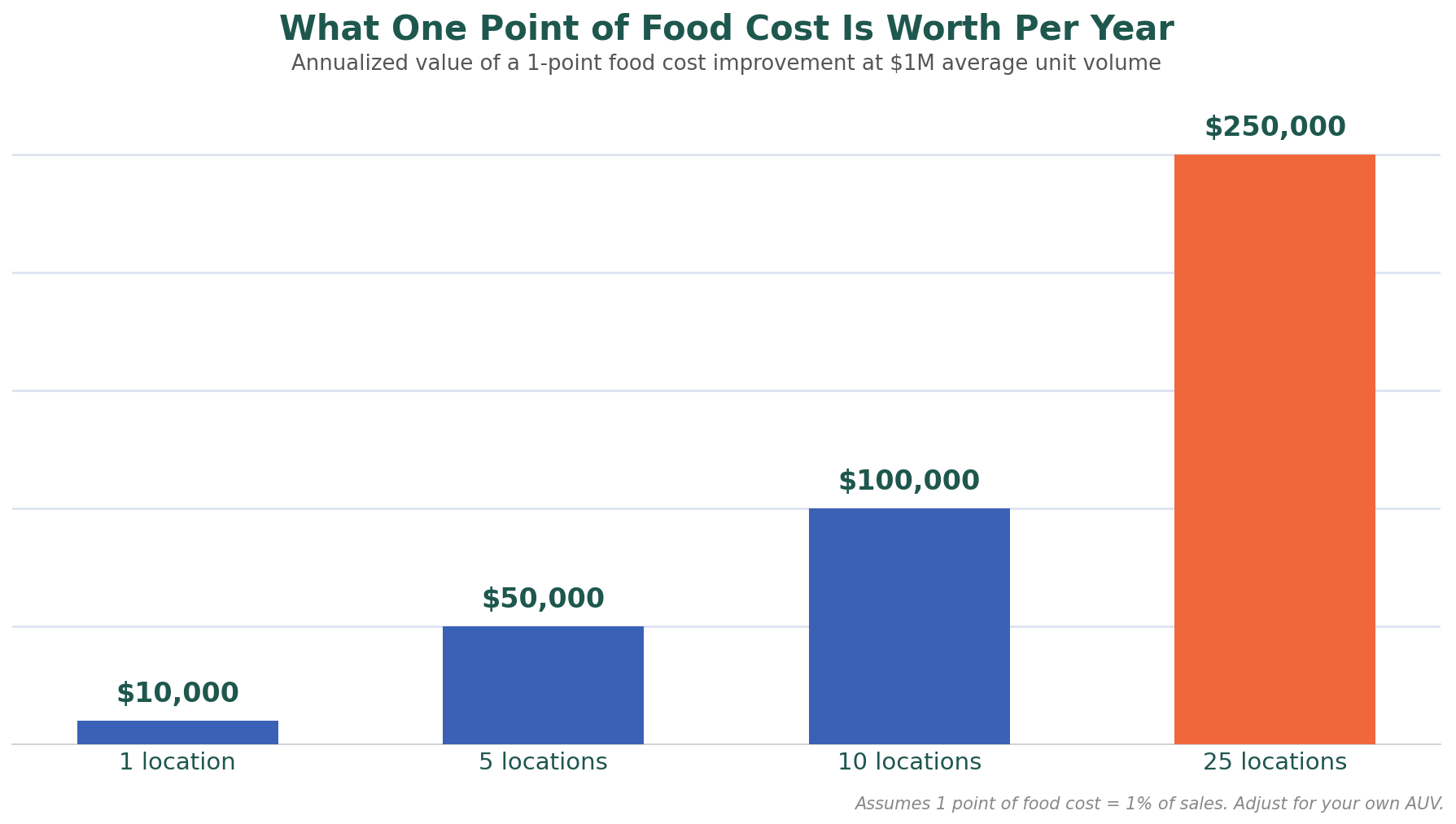

What One Point Is Actually Worth

Here is the part that should change how you think about it. Assume an illustrative unit doing $1 million in annual sales. One point of food cost is $10,000 per unit per year.

Assumptions: $1 million average unit volume, one point of food cost equals one percent of sales. Adjust for your own AUV.

At a 3 to 5 percent net margin, a one-point improvement at a single unit is a meaningful share of that unit’s entire annual profit. And unlike a one-time price concession, precision compounds. It repeats every shift, in every location, forever.

Precision Is a Margin Strategy, Not a Gadget

Buying right beats buying cheap, especially when buying cheap is no longer on the table. The distributors are not going to hand your leverage back, and beef is not getting cheaper. The operators who win the next few years are the ones who stop trying to win a negotiation they already lost, and start winning the prep decision instead, every day, in every location.

The diagnostic question for your next leadership meeting: how much of our food cost variance comes from price, and how much comes from quantity decisions we control every day?

Sources

- Federal Trade Commission, February 2015: FTC Challenges Proposed Merger of Sysco and US Foods

- Sysco Corporation, fiscal 2025 Form 10-K (market share and market size statement)

- USDA Economic Research Service, Food Price Outlook, June 2026 forecast

- USDA National Agricultural Statistics Service, Cattle report, January 2026